Looking to upgrade for investment or lifestyle? Here’s how to upgrade your HDB to a condo with our up-to-date property guide for 2023.

1. Quick Glance At The 2022 Singapore’s Property Market

Condo owners in Singapore enjoy greater status and privileges, despite being significantly more expensive than HDBs. People usually labor and save their entire lives to make the switch, but it is still daunting even when things are going well.

In 2023, downside risks persist, including high inflation, the prospect of further monetary policy tightening, geopolitical tensions and rising costs. There are also mounting concerns over slowing economic growth and a global recession. However, the Singapore residential property sector is expected to be relatively stable, supported by the underlying demand for homes and healthy market fundamentals.

Singapore’s private property market remained active throughout Covid-19. Despite the severe lack of manpower caused by extended pandemic restrictions, Singapore’s private property prices grew persistently by 5% in the fourth quarter of 2021. This is the seventh straight quarter of growth and the biggest since 2009.

So, if you’re thinking to switch to a new condo through selling your HDB, now is the time!

2. Why Are HDB Owners Looking To Buy Condos In Singapore?

The amenities are frequently the reason for upgrading from HDB to condo. Most condominiums in Singapore feature private facilities such as a gym, pool, and spa or saunas. These facilities eliminate the need to pay monthly fees or commute.

Furthermore, because these are private facilities, there are less people utilizing them than communal ones in HDB communities. If you know you’ll be utilizing the gym, pool, and other amenities frequently, the maintenance costs will be more than offset!

For individuals who have children or cherish their privacy, the security of a condo would undoubtedly be a major consideration when upgrading from a HDB. Condos have their own security measures, which make you feel safer and allow you to screen your guests.

Besides the amenities, condominiums also have a larger potential of rising in value if you choose to invest long-term. The local property market has been going higher for several decades, even demonstrating resilience during the last epidemic. Private property prices in Singapore had also increased by a stunning 53.6% between 2010 and 2020.

Although these data should be interpreted with caution because they include a wide range of private assets, the general increasing trend ensures that condo owners will witness some value appreciation.

If you’ve come this far reading the article and decided to go all-in for purchasing a new condo at this point, below is our compilation to share with you how to upgrade from a HDB to a condo smoothly and confidently.

3. How to Switch From Public To Private Housing

Before you can decide if you can afford to switch to a private condo, you must first evaluate whether you are entitled to do so. This is determined by two factors: the MOP of your HDB apartment and the EIP/ SPR Quota.

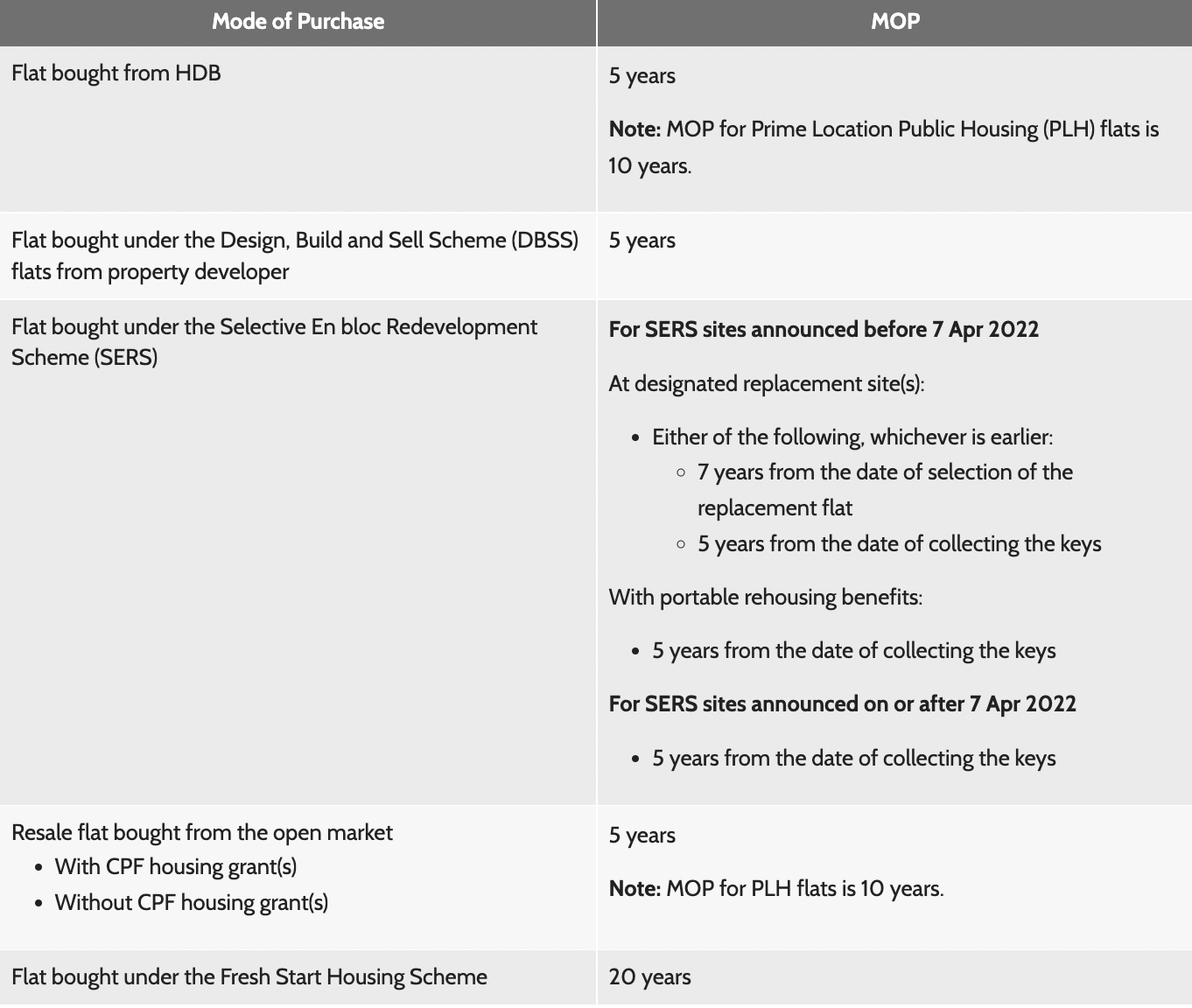

3.1. Minimum Occupation Period (MOP)

To sell your HDB apartment to switch to a condo, you must meet the Minimum Occupation Period (MOP) for your HDB unit. Typically, you must have lived in your HDB apartment for at least 5 years before you may upgrade to private property.

The MOP is based on the date you signed the Sale and Purchase Agreement for your new property, regardless of whether it is still under construction or ready for possession.

The MOP duration might vary depending on the kind of flat, therefore please consult the HBD website or our below:

HBD’s MOP duration

3.2. Ethnic Integration Policy (EIP) And Singapore Permanent Resident (SPR) Quota

The Ethnic Integration Policy (EIP) limits the total proportion of a specific ethnicity occupying a block or neighborhood. It is applied for all ethnic groups and applies to the sale and purchase of all new and resale HDB units.

On HDB’s website, there are no current EIP proportions stated. Buyers and sellers will instead have to utilize the enquiry service to see if they are qualified for the EIP.

The SPR Quota limits the overall proportion of non-Malaysian SPR households in a block or neighborhood.

The SPR Quota for non-Malaysian households is now 5% in the neighborhood and 8% in the block. It is in addition to the existing EIP limits. This implies that non-Malaysian SPRs may find it more difficult to acquire into a preferred community or block, even if they match the EIP criteria.

Under the influence of EIP and SPR, you may be eligible to sell a flat if:

- The number of residences of your ethnic group stays within the block and neighborhood borders after the sale of your unit. Furthermore, the number of non-Malaysian SPR households stays within the SPR quota.

- You and the flat buyer share the same ethnicity and citizenship.

4. The Cost To Upgrade From HDB To Condo

An apparently simple question to answer, but do you know how much it costs to upgrade from HDB to condo?

This is a whole article on its own where I explore all the different costs involved in the upgrade from HDB to condo.

Consider the following expenditures:

- Sales and cash proceeds

- Buyer stamp duty etc

- Option to purchase

- Downpayments

- Cpf payments

- TDSR

- Legal fees

- Property agent commissions

Read the full article on the Cost to Upgrade from HDB to Condo here.

5. Consider The Type Of Condominium You Want To Purchase

There are many types of condos to consider purchasing. We’ll help you decide with some keypoint comparisons.

5.1. Executive Condo vs. Private Condo

For starters, an executive condominium is a public-private hybrid. They provide the convenience of a private condominium at a government-subsidized price. They’re a profitable choice for the sandwich generation, who earn too much for a HDB but not enough for a private condominium.

In the case of private condominiums parts of the complex are held by different parties. The condominium’s common facilities, such as the garden, lobby, and gym, are shared by all unit owners.

Private condos are often built with higher-quality materials than ECs. A private condominium in a comparable area is approximately 10-20% more expensive than an executive condominium.

Here are the key distinctions between purchasing and financing an EC vs a private condo:

| Executive Condo | Private Condo | |

| Grants | ≤$30K | No |

| Price | ≤20 % Cheaper | More expensive |

| Valuation | Good appreciation | Long-term investment |

| Payment | Deferred payment scheme | Progressive payment scheme |

| Occupancy | Owner-occupancy | No restrictions |

| M.O.P | 5 years | No |

| Eligibility | First to Singaporeans only | No restrictions |

| Income Cap | $16,000 | No cap |

| Property Ownership | Cannot own other properties | No restrictions |

| Home Loan | MSR & TDSR | TDSR |

Overall, the condominium you select to buy is mostly determined by your financial capabilities as well as your intended use for the unit. If you are financially secure and the expense of a private condominium is within your budget, by all means, buy one.

If you have financial constraints, an EC may be a better fit for you. It should also be noted that private properties are more valuable in the long run if you intend to own your property indefinitely.

5.2. New Launch Condo vs. Resale Condo

There are numerous advantages and disadvantages to purchasing a new launch condo versus a resale condominium. You could go on and on about the benefits of both of these options for hours, but ultimately your decision should be based on your personal preferences.

Here is a small comparison on the top 5 pros of each property:

| New Condo | Resale Condo |

| Completely new | Opportunities to Purchase a Firesale |

| Pre-launch Discount | Available for rent immediately |

| Lower maintenance costs | Predictable Rental income |

| Various selections | Bigger unit size |

| Progressive Payment Plan Option | Less on renovation |

All in all, whether you want to invest in a resale condominium or a freshly launched condominium, you must examine your current situation. Here are some questions to help you decide:

- What is your present financial condition, and can you give payment right away?

- What are the amenities you want in the condominium, and possibly what are your plans for the house?

- Do you intend to use it only for leasing, or do you plan to utilize it for personal use in the coming years?

6. Getting Down To Your Property Sale & Purchase

After you have completed all of your investigation and calculations, the following are the procedures you must take to begin the upgrade:

6.1. Selling Your HDB

Before selling your flat, please keep in mind about

- Your potential buyers

- The asking price you’re willing to accept

- The sale proceeds after selling

- The budget and options of your next home

If you weren’t able to locate your potential buyers, you should seek the assistance of a real estate agent. You can identify your suitable agent by visiting The Council for Estate Agencies’ website.

Once you’ve spotted some of your favorite property agents on CEA’s Public Register, click ‘View more details’ to be sent to their agent page, where you’ll find:

- HDB resale records

- HDB rental records

- Private rental records

- Private resale records

The greatest part is that they will mention the location in which the property was sold, which will give you an indication of not only the sort of property they specialize in selling, but also the region in which they have sold the most properties. With this information, you can assess which agent can be of great assistance.

After that, the processes that you and your property agent will take to sell your existing HDB in order to upgrade to a condo are as follows:

- Fill out an ‘Intent to Sell’ form on the HDB website.

- Calculate the sale and cash profits of your apartment.

- Begin promoting your home for sale.

- Give the customer a $1,000 option to purchase (OTP).

- Wait for the buyer to use the OTP for an additional $4,000

- Submit the HDB resale application.

- Approve the resale documentation

- Pay the applicable costs online.

- Receive the sale’s approval

- Attend the HDB selling appointment.

In general, it takes around 8 weeks from the submission of the selling documentation to the appointment with HDB.

However, keep in mind that there will be an escrow period before the payment is locked in and final. The solicitor is in charge of establishing and administering the escrow agreement and ensuring that the terms and conditions are in place and that particular timetables in the property transaction are followed. These clauses generally encompass everything from the property’s timely completion to any interest payable at various phases of development.

After everything is in order, the monies in the escrow account will be transferred to you, the seller, and the transaction is officially finished.

As the numbers above show, transaction volumes in the public resale home market have slowed in recent quarters. The number of millionaires created through the sale of HDB houses is expected to grow at a slower rate, especially as former and present private property owners would now have to wait 15 months before acquiring a HDB resale unit. Demand for resale HDB apartments will be dampened. As a result, if you still want to make more money from the sale, we recommend that you act promptly and carefully.

7.2. Buying Your Condo

There are several variables to consider when purchasing a condo in Singapore. Ultimately, selecting the best one comes down to your own tastes; take some time to think about what your priorities are before taking the plunge to land your dream house. Here are some key points to bear in mind:

- Ensure you can afford the 25% down payment.

- Determine if the unit is freehold or leasehold.

- Explore neighboring MRT and transportation lines.

- Check the amenities to determine if you’d actually use them.

- Set up money for taxes and stamp duties.

- Confirm to see if the condo’s size is appropriate for your future goals.

- Test whether the measurements of the showflat are close to yours.

- Consider the advantages and disadvantages of each unit location.

After that, it will be simple considering buying takes significantly less time than selling. You should follow the steps listed below with your real estate agent (condo purchasers are not required to pay their real estate brokers, so you may utilize this service for free).

- Begin looking for units to buy and ask the condo owner for a 1% OTP.

- Obtain legal counsel and finalize your loan.

- Use the 4% OTP and pay the stamp duty

- Sign the Sale and Purchase contract.

- Transfer responsibility to your attorneys.

- Pay the remaining 20% of the down payment.

And if you are purchasing a new launch condo:

- List your best selections.

- Look at showflats

- Pay the 5% (Cash) booking cost to reserve a unit

- Obtain legal counsel and finalize your loan.

- Pay the stamp duty when exercising the OTP.

- Sign the Sale and Purchase contract.

- Pay another 15% downpayment due 8 weeks after the booking date.**

- When TOP is granted, pay the remaining 40%

**Subsequently, a 5% downpayment must be paid upon reaching the foundation stage of construction. The rest of the 75% purchase price can be paid via a bank loan (subject to eligibility based on income and TDSR calculations and maximum 75% LTV)

8. The Ultimate Decision: Buy or Sell first?

Buying the condo first or selling the HDB first has a considerable influence on how you finance your new condominium.

There may be times when purchasing the condominium first makes more sense for you. For example, you may have located a condo that meets your criteria and wish to secure it before others do. Or perhaps you do not want to deal with the inconvenience of obtaining temporary housing during the move.

In any case, the last thing we want is to have lost the intended unit because we waited to sell the HDB first or sold first only to discover that there is nothing you intend to buy.

If you purchase the condo first, you will be subject to the terms of a second mortgage for your Loan-To-Value (LTV) and cash down payment.

You would also be subject to Additional Buyer’s Stamp Duty, as previously stated (ABSD). You do not have to pay ABSD if you have agreed to sell your sole unit (HDB) before signing the Acceptance to Option to Purchase for the condominium. If you have not committed to sell your flat, your condominium acquisition will be your second property, for which you must pay ABSD according to your unique circumstances.

Unlike private property, where decoupling may be widespread to prevent ABSD, HDB decoupling has been limited since April 1, 2016. Decoupling of HDBs is only permitted under certain circumstances, including marriage, divorce, the death of an owner, financial difficulties, loss of citizenship, and medical grounds.

When you upgrade from a HDB apartment to a private property or buy another private house, you must pay ABSD in cash or CPF up front (within 14 days of signing the Sales and Purchase Agreement). If you sell your first property within six months, you can apply for an ABSD remission (subject to terms and conditions to be eligible for ABSD remission).

When purchasing a new EC, you can avoid paying ABSD up front. You must sell your property within six months of receiving the keys to your EC (or when your EC obtains its Temporary Occupation Permit), but at least you are not required to pay the hefty ABSD charge at the outset, though, you may need to pay the HDB resale levy.

If you decide to sell your HDB first or have already done so, the situation would be simpler. There would be no ABSD, and you would be eligible for a larger loan amount since you meet the criteria for a “first housing loan” in terms of Loan-To-Value (LTV) and cash down payment.

We will review the possibilities in further detail so that you can make an informed decision.

Plan 1: Buy Then Sell

You can acquire the condo of your dreams before selling your HDB apartment if you have enough funds to pay for the ABSD as well as the higher downpayment (55% of purchase price). As the condo is deemed their second property, they will have to pay an extra buyer’s stamp duty (ABSD) of 17%. That’s $170,000 on a $1 million condo.

But there is a catch! Married couples who sell their HDB apartment within 6 months of purchasing the private property, can apply for ABSD full refund. However, this criterion is rather stringent, and no extensions are permitted.

Another thing to think about is your loan-to-value ratio. You will only be allowed to obtain a 45% bank loan to service your mortgage on your second home acquisition. If you have previously paid off your first HDB mortgage, you can continue to loan up to 75% of the value of your apartment as usual.

Plan 2: Sell Then Buy

Another option for considering the move is selling their HDB before purchasing a condo. Those who pick this option will not be required to pay any ABSD because their “new” unit will be deemed their first property. There would also be no pressure to sell their HDB within the next six months to qualify for the ABSD return. However, there are some minor drawbacks.

You’ll need to locate temporary housing with your parents or by renting a flat. The former will save you some money on rent, but you’ll have to relocate twice, which might be inconvenient.

By delaying the sale of your HDB, you risk missing out on the ideal apartment you’ve been eyeing. Waiting for a comparable condo to come on the market will mean spending time away from your place.

Plan 3: Buy & Sell All At Once

The third option is for people who can afford both an HDB apartment and a condo simultaneously, on top of all fees and mortgages. If you don’t mind paying the hefty 17% ABSD, the world is your oyster, and you can have two homes.

You might also rent out one of the residences to help pay down the mortgage. Here are the prices for you to refer to, derived from HDB.

Conclusion:

Consider your financial and personal objectives, as well as how they all fit into your timeframe, to determine whether it is right for you to upgrade from HDB to a dream condominium.

If you have any specific questions regarding your exact situation that you can’t find the answers to anywhere else, feel free to ask me anything.